- Investors are cautious ahead of US jobs data and major companies’ earnings reports.

- US second-quarter earnings are predicted to fall 5.9% from the previous year.

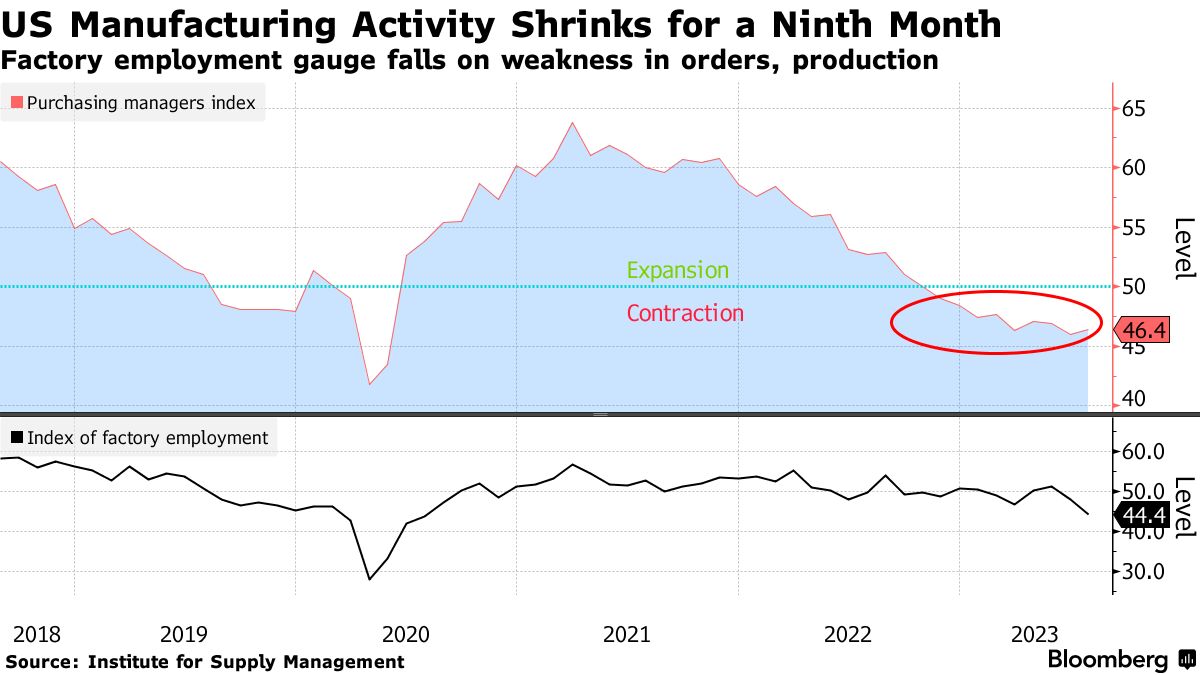

- US manufacturing stabilized at lower levels in July, gradually improving new orders.

On Tuesday, US equities closed weaker, marking the start of the seasonally slow August. Investors were cautious ahead of US employment data and major companies’ earnings reports later this week.

Shares of mega-cap growth companies like Tesla and Amazon.com, whose valuations suffer when borrowing costs rise, declined as the benchmark 10-year US Treasury note yield surged over 4%.

July ended positively for US equities as investors celebrated better-than-expected earnings. The economy remained resilient, and hopes of a soft landing were boosted by cooling inflation and rising interest rates. The benchmark S&P 500 hit a 16-month high on Monday and is now less than 5% away from its record-high closing level set on Jan. 3, 2022.

Scott Ladner, the chief investment officer of Horizon Investments, mentioned that historically, August has been a weak seasonal month. Hence, some investors took the opportunity to reduce their positions slightly.

Meanwhile, Refinitiv data on Tuesday showed that US second-quarter earnings are now predicted to fall 5.9% from the previous year, an improvement from the last estimate of a 7.9% decline.

US manufacturing activity (Source: Institute for Supply Management)

On the data front, US manufacturing stabilized at lower levels in July, with new orders gradually improving. However, factory employment dropped to a three-year low, suggesting that layoffs were increasing.

European equities also faced losses on Tuesday, with the German DAX retreating from record highs. Shrinking factory activity in the Eurozone, China, and the United States, indicated growing risks to the global economy from rising interest rates.

A survey showed manufacturing activity in the Eurozone contracting at the fastest pace since May 2020 as demand slumped, despite factories reducing their prices significantly.

Germany, Europe’s largest economy, experienced considerable weakness, while France and Italy, the second and third-largest Eurozone economies, also recorded significant deteriorations.

Speculation about the Federal Reserve and the European Central Bank nearing the end of their tightening measures and positive earnings had supported gains in the STOXX 600 in July. Analysts now expect a 5.8% contraction in quarterly profit for STOXX 600 companies, an improvement from the 8.1% decline seen last week.

Meanwhile, the UK’s FTSE 100 experienced a decline due to a drop in mining firms’ shares following China’s contraction in manufacturing activity in July.