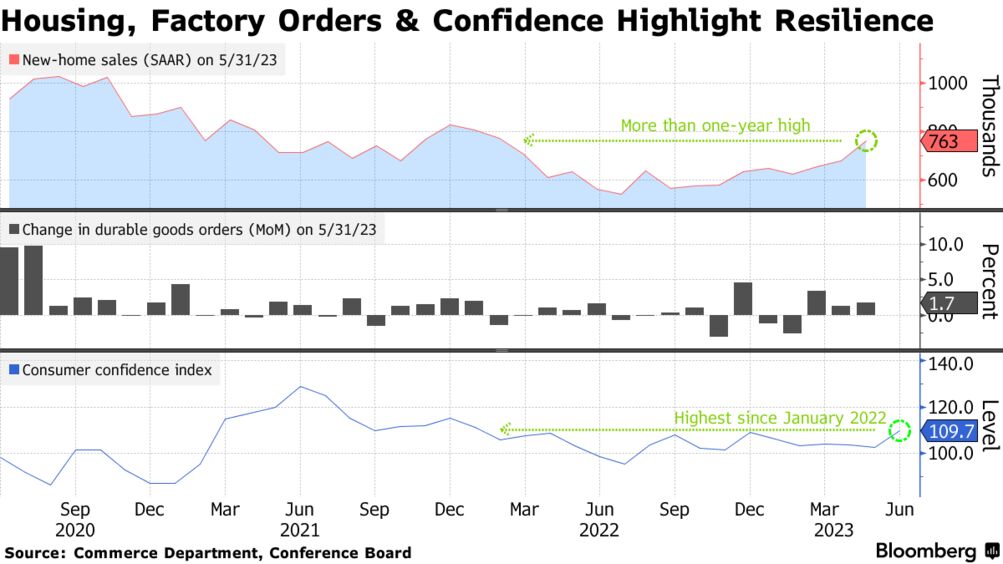

- New orders for important US-manufactured capital goods unexpectedly increased in May.

- US consumer confidence reached a nearly 1-1/2 year high in June.

- Investors expect further policy stimulus from China.

On Tuesday, US equities recovered from a losing streak due to positive economic data. This eased investor concerns about an impending recession caused by the Federal Reserve’s aggressive interest rate increases.

US housing, factory orders and confidence data (Source: Commerce Department, Conference Board)

In May, new orders for important US-manufactured capital goods unexpectedly increased, and sales of new single-family homes surged. Additionally, US consumer confidence reached a nearly 1-1/2 year high in June.

Mark Luschini, a chief investment strategist at Janney Montgomery Scott in Philadelphia, stated that the data gave investors a reason to reinvest in stocks following a significant downturn in previous sessions.

Rhys Williams, the chief strategist at Spouting Rock Asset Management, mentioned that while the economic data was encouraging, the market was likely influenced by “window-dressing.” This is where fund managers add outperforming assets to their portfolios for end-of-quarter statements.

According to CME Group‘s Fedwatch tool, traders estimated a 77% chance that the Fed would raise interest rates by 25 basis points to the 5.25%-5.50% range during its July meeting. This was slightly up from the previous day’s 74.4%.

This week, more economic data is expected, including a crucial inflation measure and a speech by Fed Chair Jerome Powell at the European Central Bank Forum in Sintra.

Powell’s hawkish remarks last week halted a stock rally in the US that had propelled the S&P 500 and Nasdaq to their highest levels in over a year and the Dow to a six-month peak. Despite the recent market weakness, a rally in growth stocks, a positive earnings season, and hopes of the Fed concluding its monetary tightening soon have put the main indexes on track for quarterly gains.

European equities rose on Tuesday, driven by financials and luxury stocks, as investors speculated on further policy stimulus from China. However, gains were limited by hawkish comments from European Central Bank President Christine Lagarde.

China’s Premier Li Qiang stated that the country’s economic growth in the second quarter would surpass that of the first quarter and is expected to reach the annual economic growth target of approximately 5%. These comments relieved investors recently concerned about smaller-than-anticipated rate cuts in China, political instability in Russia following a failed mutiny, and the possibility of an extended global interest rate hiking cycle.

{kind=link}