- The S&P 500 is trading near two-month highs as investors wait for a flood of earnings.

- US interest rates are anticipated to rise by 25 basis points.

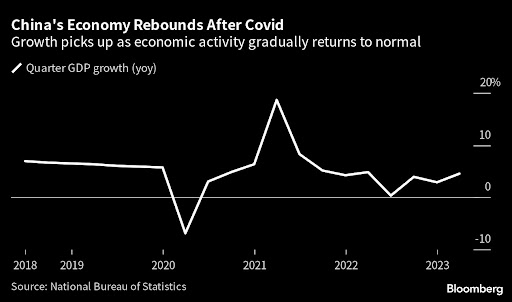

- The Chinese economy expanded by 4.5% in Q1 from the previous year.

Equities in the US and Europe made some gains on Tuesday as the first-quarter earnings season started. The S&P 500 scraped out a tiny gain thanks to the resilience of a few large technology firms, which helped offset weaker-than-expected quarterly results from Johnson & Johnson and Goldman Sachs.

Shares of healthcare firm J&J dropped 2.8% after it warned investors about the lingering effects of inflation-driven prices this year. Shares of Goldman dipped 1.7% after the Wall Street company reported a 19% decline in profit due to weak dealmaking and bond trading.

Investors have been preparing for a somber reporting season since they believe the economy is about to enter a slump.

The S&P 500 is trading near two-month highs as investors wait for more earnings and evaluate the interest rate outlook before the Federal Reserve’s meeting early next month. Interest rates are anticipated to rise by 25 basis points.

St. Louis Federal Reserve president James Bullard told Reuters on Tuesday that the US central bank should keep hiking rates in light of recent statistics showing persistent inflation. In a different statement, Raphael Bostic, president of the Atlanta Federal Reserve, indicated that the Fed would raise rates again.

European equities ended the day higher on Tuesday. Better-than-expected economic statistics from China improved demand forecasts and increased shares of miners and luxury companies. Travel and leisure sectors led the rally on stronger earnings.

After the tight COVID-19 limitations were lifted in December, the Chinese economy expanded 4.5% year over year in the first quarter, exceeding expectations. However, the strength of domestic demand is being questioned in light of reducing inflation and rising bank savings.

Refinitiv data predicts that STOXX 600 businesses’ first-quarter earnings will decline 2.5% from the previous year. Up until Tuesday, four STOXX 600 businesses announced earnings, and 75% of those companies exceeded earnings expectations.

Bank stock prices ended the day 1.3% higher, reversing most of the previous day’s losses.

After a difficult month, the outlook for lenders has brightened as concerns about the banking sector have lessened. There are indications that inflation is slowing, and policymakers at the European Central Bank have been generally hawkish in their remarks.