- Nearly one-third of S&P 500 companies will report results this week.

- Out of the 118 S&P 500 companies that have reported so far, 81% have exceeded analysts’ expectations.

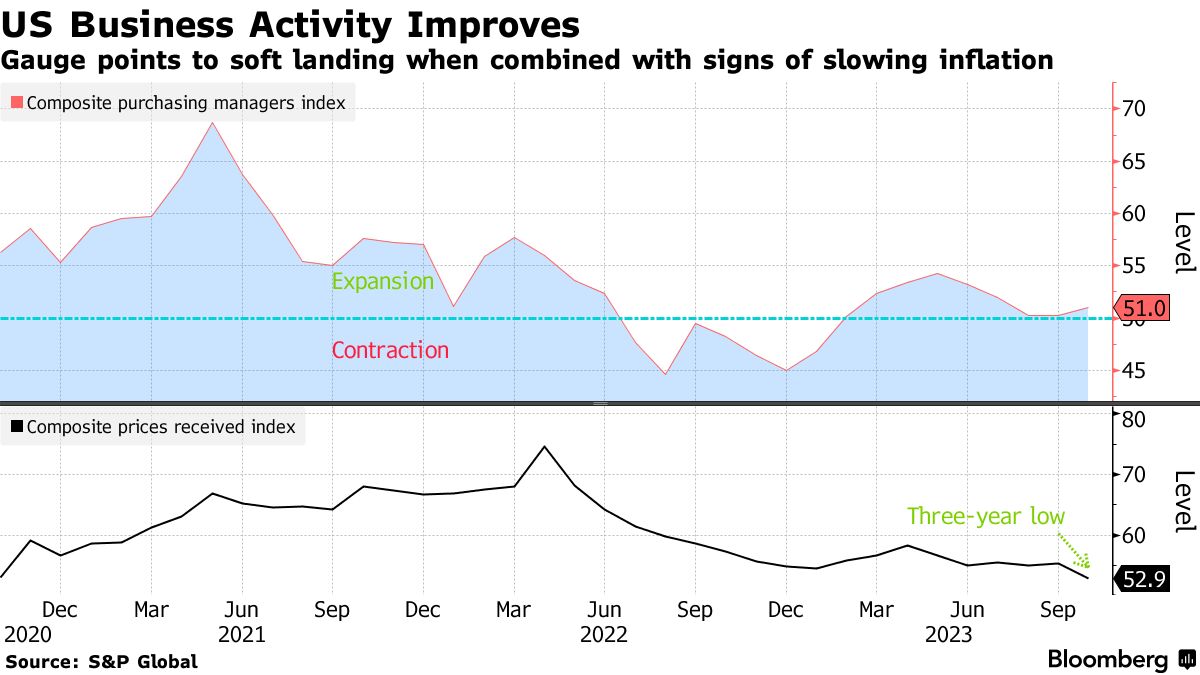

- Business activity in the US improved this month.

On Tuesday, equities rose thanks to strong corporate earnings and optimistic forecasts, boosting investor risk appetite and sparking a broad market rally. All three major US stock indexes moved higher, largely driven by large-cap companies sensitive to interest rates. Meanwhile, benchmark Treasury yields remained stable, comfortably below their recent peak at 5%.

The third quarter earnings season is in full swing, with nearly one-third of S&P 500 companies reporting results this week. According to Thomas Martin from GLOBALT in Atlanta, the earnings reports had been somewhat disappointing before the last couple of days. Still, this week has brought more positive and better earnings.

Notably, out of the 118 S&P 500 companies that have reported earnings, 81% have exceeded analysts’ expectations, as per LSEG.

US business activity (Source: S&P Global)

On the economic front, business activity in the US has improved this month, with the manufacturing sector recovering from a five-month contraction due to increased new orders. Moreover, services activity showed a modest acceleration with signs of easing inflationary pressures.

Looking ahead, the Commerce Department will release its initial estimate of third-quarter GDP on Thursday, expected to show a strong acceleration to 4.3% from the 2.1% growth in the second quarter.

Additionally, on Friday, the Commerce Department will publish its closely monitored Personal Consumption Expenditures (PCE) report. Analysts believe it will provide further evidence of a gradual decrease in inflation toward the Federal Reserve’s target rate of 2%.

In European equities, despite concerns about lackluster economic data in the Eurozone, robust earnings from the region and the US led to gains on Tuesday. However, financial institutions faced a setback, with lenders down 1.0%. Barclays fell 6.5% as it hinted at significant cost-cutting later in the year and expressed concerns about competition for savers’ deposits impacting its margins.

Spanish bank stocks also declined due to uncertainty about a potential profit reduction. This forecast is due to calls to increase a windfall tax in a coalition government agreement between Spain’s leftist platform Sumar and the Socialist Party.

Furthermore, data revealed that the Eurozone Composite Purchasing Managers’ Index (PMI) hit a nearly three-year low in October. Moreover, business activity in Germany contracted for the fourth consecutive month, raising concerns about a possible recession.