{kind=link}

The equity market worldwide made records high in the recent past. The cause of this performance, lately, is the support offered by the corporate earnings report which showed a better performance than what was earlier projected due to the authorization of the COVID-19 rescue package in the European Union (EU) and anticipations that the US Congress will later arrange a supplement fiscal policy.

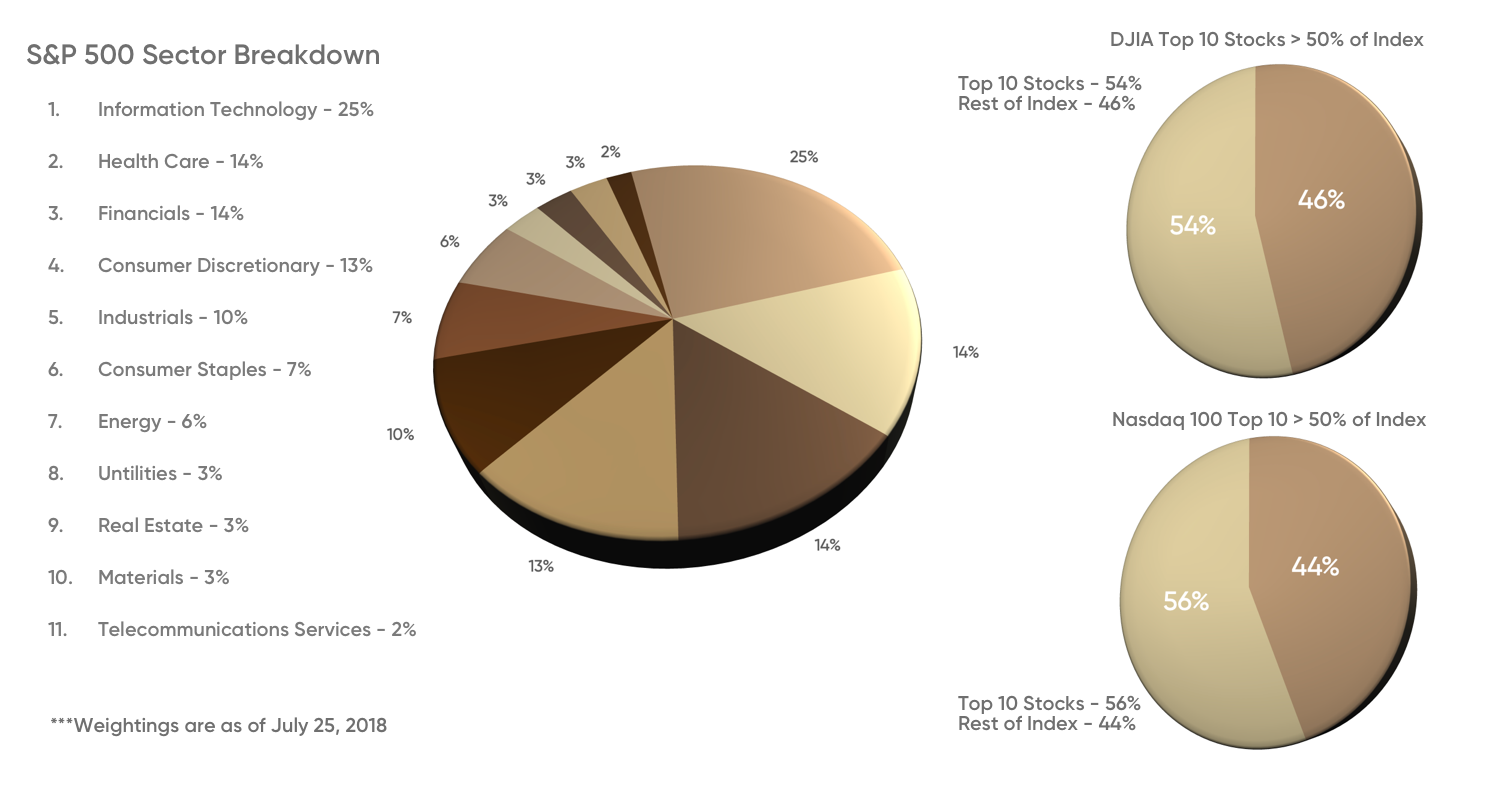

Although European equity markets were lagging because of the rise in Euro price, US equity indices like the S&P 500 index and the Nasdaq 100 index made fresh all-time highs in the beginning of September. The eventual correction was not activated by a fall of liquidity or a policy alteration and is thus viewed as a positive move. The bull market in equity markets is still leading.

Despite the recent improvement in the leading indicators, the additional comeback of losses in gross domestic policy will prove more tasking, and beginning from now, it will be more varied and unrelated going forward.

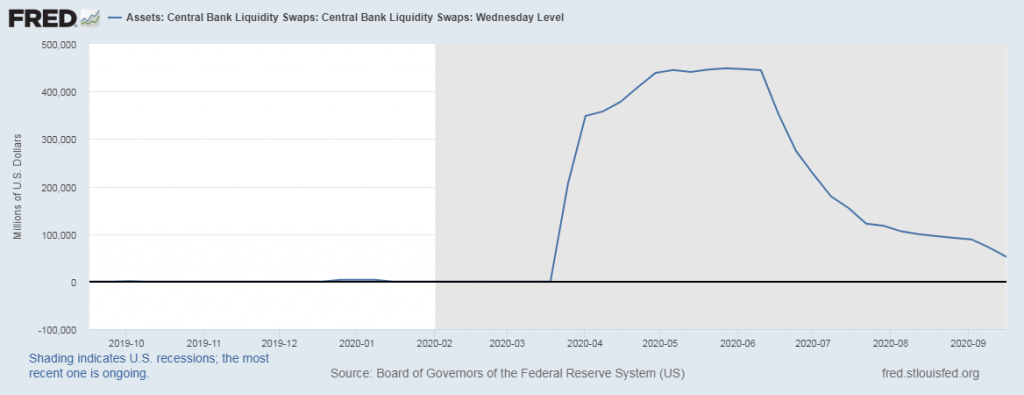

The US Central Bank Liquidity Measure

The Central banks’ liquidity measures would continue to provide support for the predictable future. Thus, fiscal policy will be the main policy variable from now. For that reason, the primary risk in markets, currently, is an untimely pulling out of fiscal incentive instead of the unwarranted public debt.

Analytically, Central Banks need to regularly renew fiscal support processes as opposed to the renewal of monetary support, until such a time the private sector fully recovers with the capacity to maintain enough demand. If this is not done, it could result in the stagnation of the economy.

The forthcoming presidential election in the US which was scheduled for the 3rd of November, 2020 is the most essential political event from now onwards till the end of 2020.

The recent devaluation of the US dollar is not the beginning of a price fall against other fiat currencies. The fall is mostly against the euro, which gained immensely from the EU recovery fund agreement.

Additional Fiscal Incentives Are Essential

The cool phase of the economic rebound which occurred during the lockdown has come to an end. Going forward, it will be harder to recover the lost gross domestic product (GDP). It’ll also no longer be homogenous.

Because of the return of Covid-19 cases in a few locations, which in turn resulted in sensible actions or quarantine procedures, closing the output gap will take a lot more time. And getting back to the 2019 GDP levels of economic activities in top global economies apart from China will take a while. Although the vagaries of the COVID-19 obvious make the whole situation more complicated, due to the potential that a drug or vaccine could suddenly change the swings of things in a twinkle of an eye.

In the current situation of the economy, central banks are supposed to take an accommodative approach for a few years to come. The key risk for different world economies, thus, is the untimely removal of monetary incentives. Contrary to fiscal policy, which continues to be maintained until it is vigorously altered by central banks, fiscal stimulus ought to be transformed from time to time until the private sector can maintain enough growth levels.

In the face of the present COVI-19 scenario, governments ought to figure out new ways to additionally prove supportive to families and private businesses. If the government wants to reduce public-sector demand, it will activate a fresh economic tightening.

The New Fed Approach To Inflation Could Further Affect The Dollar Rate

The chairman of fed, Jerome Powell made a recent announcement of a key policy shift to “average inflation targeting.” What this implies is that the central bank is willing to let the inflation move above the 2% target which is the accepted standard before they can hike the interest rates. This is to offset the moves it made when the rate fell below the 2% level.

Coupled with the change in inflation, the Fed altered its employment strategy in a manner that centers much more on individuals with lower income levels. The Federal Reserve wants to do this to provide support to the job market and the overall economy.

Fed chairman, Jerome Powell, termed the move a “robust updating” of Fed policy. That was the formal announcement by the central bank to adopt an “average inflation targeting” policy. The recent move was added into the policy code referred to as the “Statement on Longer-Run Goals and Monetary Policy Strategy,” which was originally adopted in 2012. It was from this policy that the Fed’s approach to interest rates and the overall growth of the economy emanated.

Fed Gradually Moves away From The Old Fiscal Policy

Practically, what the movement implies is that the Fed would be less likely to increase interest rates if the rate of unemployment gets lowers, in so far as the rate of inflation doesn’t equally rise. Officials of the Central bank think that a fall in the rate of unemployment, commonly results in excessively high inflation and so they have taken the preventive action.

Nonetheless, the speech delivered by Powell to an online meeting of the Fed’s annual Jackson Hole, Wyoming, conference, and associated documents that were included in the fresh policy code, showed that the Fed is moving away from the old fiscal policy. And the change was collectively endorsed by the Policymaking Federal Open Market Committee.

A lot of people think that the recent move and inclination of the Fed to cause inflation increase is counterintuitive. But, Power in his reply said that when the rate of inflation constantly remains very low, it could hurt the economy.

At first, there wasn’t a strong reaction against his remark, however, the stock market futures soon made a record high, and the following morning, there was an increase in key averages. Powell indicated that if the interest rate level doesn’t either go up to push growth or move down greatly down the years and it’ll potentially remain there.

He differentiated the present scenario to what happened to the Fed last 40 years, when Paul Volcker, who was the then-Fed chairman, implemented a rage of provocative interest rate hikes to force inflation down. In the past, basic alterations in the economy, like a tech change or change in demographics has caused the Fed to move away from very low inflation.

According to Powell, the current scenario can result in a long-term risky fall in inflation outlooks and when this happens, it could additionally lower the rate of inflation and leads to a distasteful continuous cycle of lower inflation and inflation outlooks. In the end, the situation will give the policymakers small room for lowering interest rates when the economy is under pressure.

Starting from the financial crisis culminated, the Fed has been struggling to maintain its 2% inflation target. Fed officials anticipate that the recent approach would alter the scene and raise expectations while increasing inflation even as the rates continue to fall.

Although Powell did not mention how high they want to increase the inflation, Dallas Fed President Robert Kaplan afterward mentioned in a CNBC interview that they’d be looking at roughly 2.25 – 2.5 percent inflation.

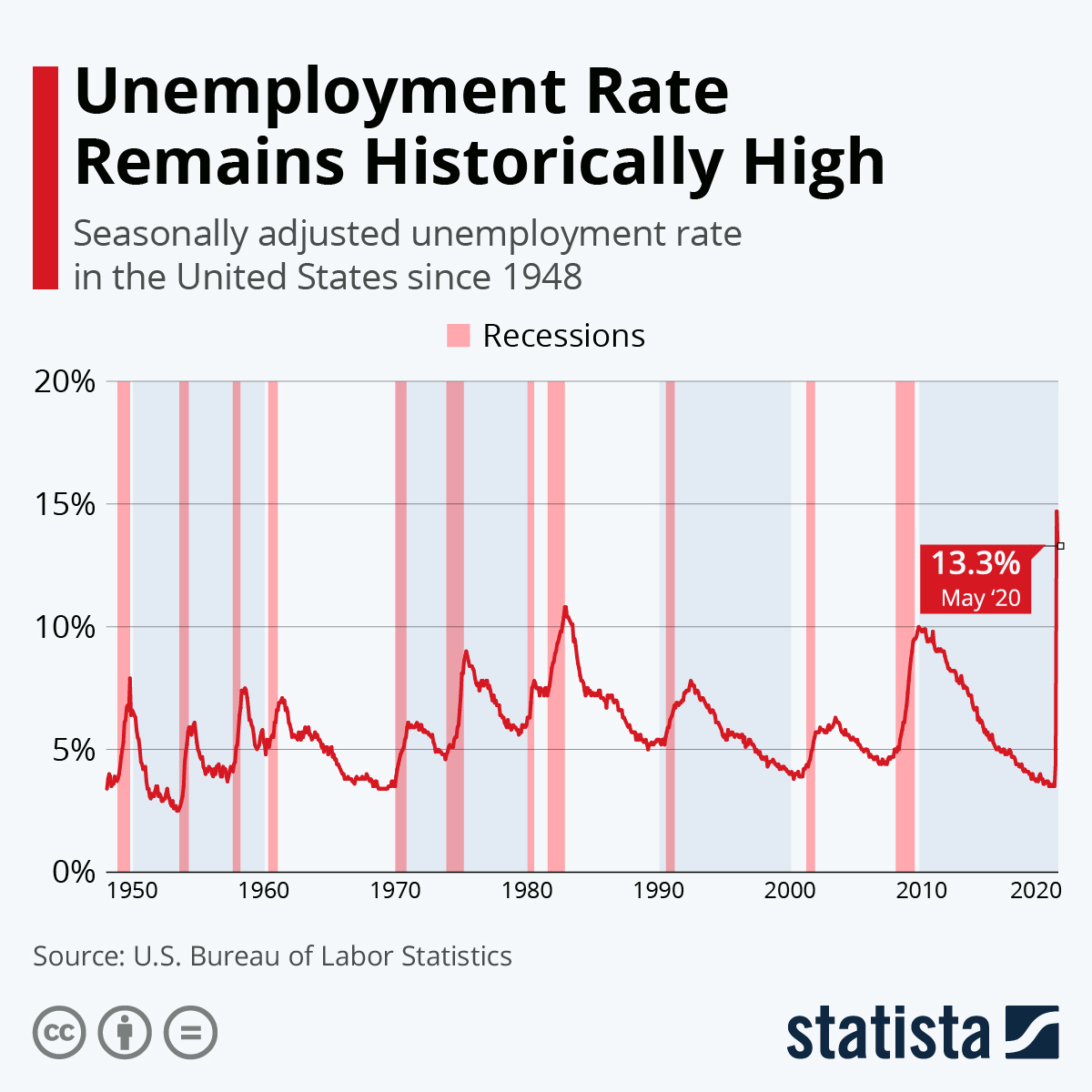

While the current unemployment rate is well above 10%, the likelihood of a resultant high inflationary rate short-term is slim. Whether or not the Fed makes the policy change, the Federal Reserve would remain at a zero position for a few years to come.

Employment Policy Shift

Besides the inflation ship, the Fed equally declared its intention to tweak employment policy. While it appears only to be mere talks, the Fed chairman noted it would be a significant move. The present Job market approach will depend on the Fed’s “assessments of the employment deficits from the maximum level.” The previous term is known as “deviations” from the maximum level.

The new move represents the Fed recognition of the advantages of a robust labor market, especially for a lot of low- and moderate-income communities. The FED chairman further said that the new move indicates how they think that the maintenance of a robust job market is possible without any form of inflation outbreak.

The Fed is mostly concerned about citizens who are hardly hit by the impact of the coronavirus pandemic. Therefore, the language change is a way to manage the situation pending the time the economy fully recovers.

According to Powell, the Fed is not planning to set fixed unemployment. They’d rather allow the market conditions to dictate what the full employment would be. The earlier projections of the FED anticipated that inflation would move higher than the 3.5% generational low which was the level of unemployment before the Covid-19 incidence. However, that was far from reality. Powell noted that the Fed continues to hold the 2% inflation rate as a suitable long-term target.